While passive hedging can effectively lower currency risk in international portfolios, the negative interest differential between Switzerland and the United States has hurt Swiss investors as US investments typically dominate foreign allocations. This has led to a need for innovative strategies within hedging to alleviate carry penalties while managing currency risk. One such approach, where Mesirow has exceled, is tenor management.

With Switzerland allocating most of their equity and bond investments overseas, currency risk continues to be a major source of risk for pension plans. Currency overlay managers such as Mesirow have the expertise to manage this risk for Swiss investors. For risk averse investors, passive hedging offers a solution that effectively reduces currency risk in the international portfolio.

Due to the negative interest differential between Switzerland and the US, passive currency hedging inflicts a carry penalty for Swiss investors hedging US dollar. With the current rates of Switzerland and the US at 1.75% and 5.5% respectively (as of this article's publication, January 2024), the carry penalty associated with hedging the US dollar is not insignificant. Therefore, while passive hedging is a solution that reduces currency risk, the cost associated with hedging remains a burden.

While maintaining the prescribed level of currency risk in the portfolio remains the priority, the structure of hedging allows for choice of forward contract length, i.e., tenor selection. Fixed interval value dates are often used to simplify operational complexities, e.g., fixed 3M contracts result in settlements and cash flows on a fixed quarterly interval. For investors who have high cash flow and liquidity sensitivities, staggering multiple contracts can help reduce cash flow volatility while maintaining the same fixed payout interval, e.g., 2 fixed 6M contracts each covering 50% of the exposure, staggered 3 months apart. For investors who prioritize a return boost over operational complexities, while maintaining the desired level of currency risk, selecting optimal tenors through tenor management can achieve this goal.

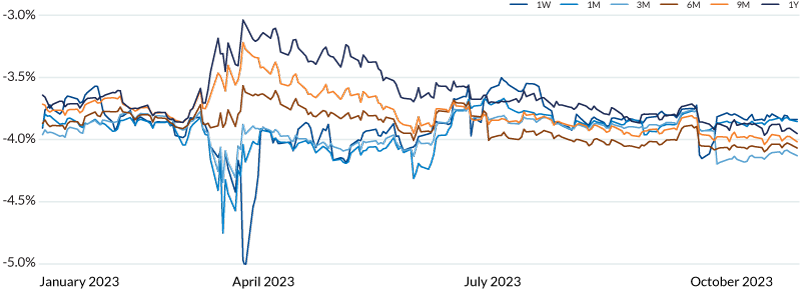

To illustrate this opportunity through tenor selection, durations from 1 week through 1 year are displayed in the following charts, revealing that carry penalties vary over time. For Swiss investors, higher negative carry equates to a higher penalty to hedge.

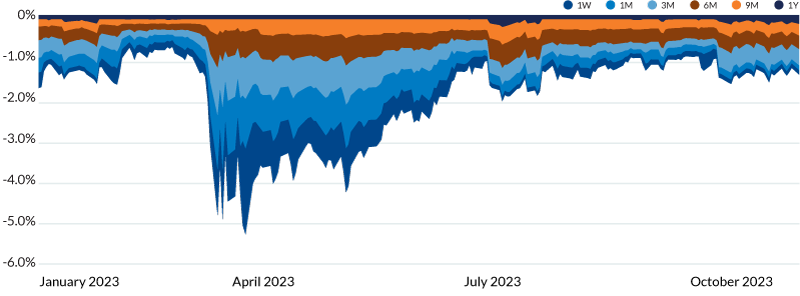

In 2023, the annualized carry penalty across various tenors differed up to 2% at times (figure 1), with the lower lines representing larger magnitudes of carry penalty while the higher lines represent smaller magnitudes of carry penalty. The relative differences between tenors are more obvious when stacked in an area chart (figure 2), where the smaller areas represent less carry penalty relative to other tenors. In 2023, the longer end of the curve has been smaller and less variable this year, whereas the shorter end of the curve has been larger and more volatile.

A disciplined tenor management strategy with structure, process, and systematization can determine the optimal tenor length for hedging, reducing the carry penalty while effectively managing the currency risk in the portfolio. A full-service provider of FX strategies and products such as Mesirow offers expertise and tailored hedging solutions, such as tenor management, to manage currency risk across a spectrum of strategies from passive to active management.

Mesirow also partners with Perreard Partners Investment in Switzerland, who provide valuable in-market expertise, delivering locally based service to Mesirow currency clients.

Connect with us to learn more about Mesirow Currency solutions

Customized solutions to manage unrewarded currency risk in international portfolios.

Strategies that aim to profit from short and medium-term moves in the currency market.

Trading solution for asset managers and owners with focus on reducing transaction costs, improving transparency and enhancing efficiency.

The information contained herein should not be construed as a recommendation to purchase or sell any particular security or investment vehicle offered by Mesirow . The information included has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Mesirow Financial Investment Management, Inc. and its affiliated companies and/or individuals may, from time to time, own, have long or short positions in, or options on, or act as a market maker in, any securities discussed herein and may also perform financial advisory or investment banking services for those companies. It should not be assumed that any recommendations incorporated herein will be profitable or will equal past performance. Any stated performance results include the reinvestment of dividends and other earnings. Investment management services offered by Mesirow Financial Investment Management, Inc., an SEC-registered investment advisor.