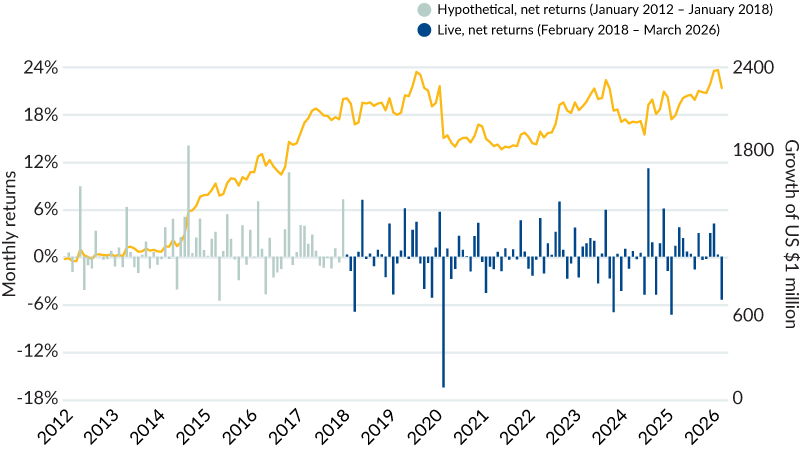

Currency for return

Mesirow Currency has delivered innovative, customized currency solutions to institutional clients globally since 19901 and is fully aligned with client interests. As a private, employee‑owned firm, we avoid many conflicts commonly associated with bank‑affiliated or publicly traded firms.

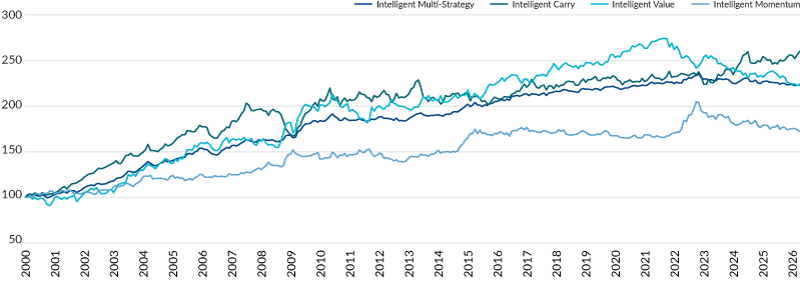

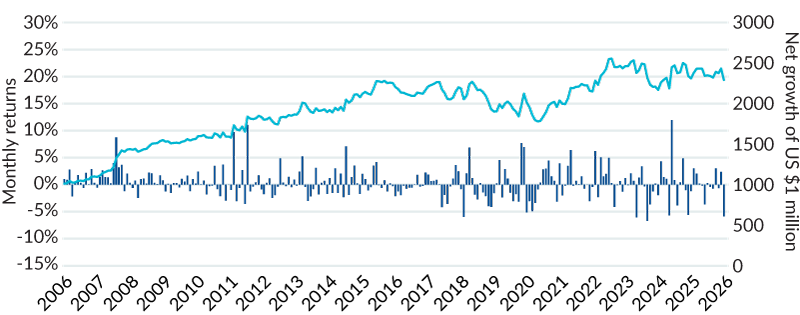

(Hypothetical Returns, January 2000 – November 2020 | Live Returns, December 2020 – March 2026)

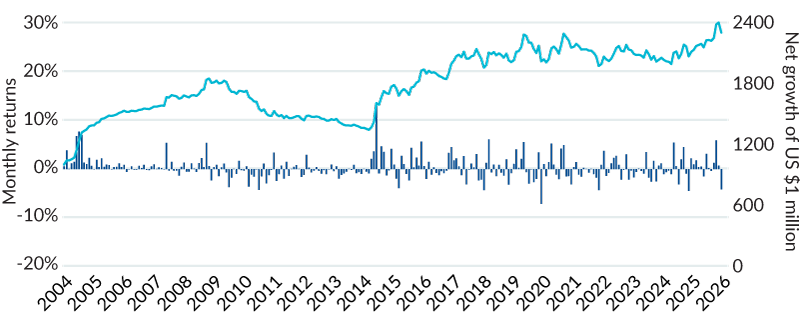

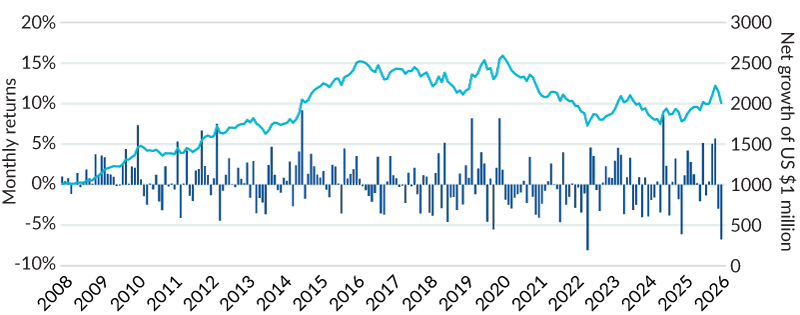

(Hypothetical Returns, January 2000 – November 2020 | Live Returns, December 2020 – March 2026)